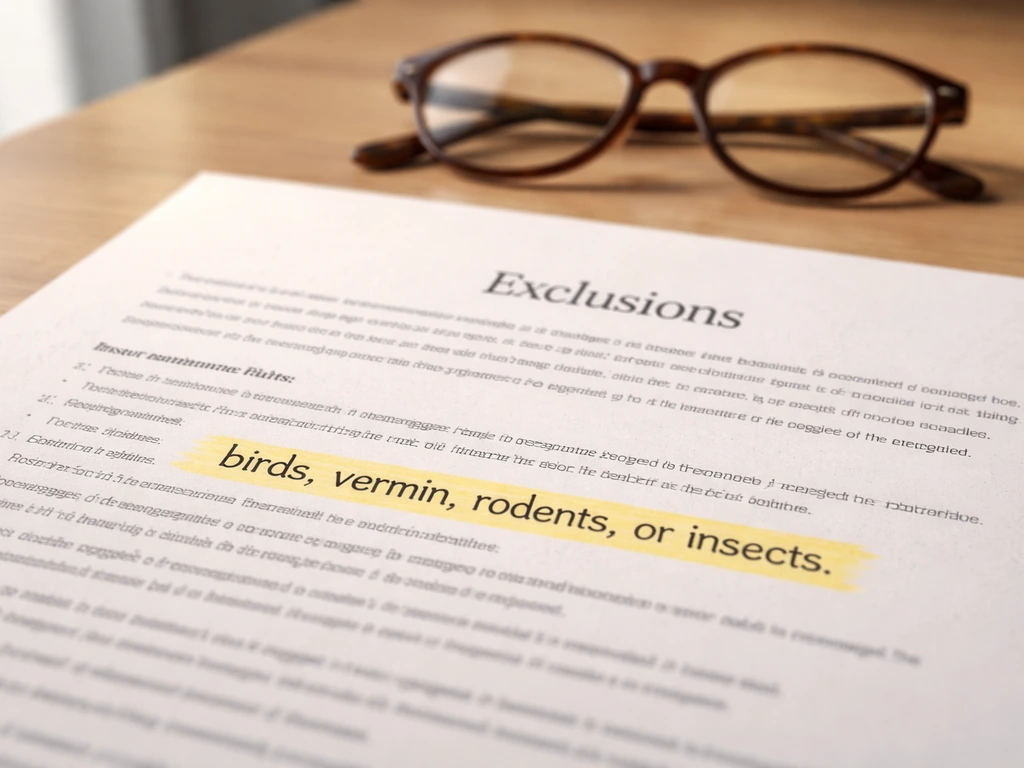

Most bird damage is not covered by a standard homeowners insurance policy. The ISO HO-3 and HO-5 forms that most insurers use include an explicit exclusion for damage caused by 'birds, vermin, rodents, or insects,' and that exclusion is the first thing an adjuster will point to when you file. That said, there are real scenarios where bird-related damage can slip under a covered peril, and knowing the difference can save you a lot of back-and-forth with your insurer.

Is Bird Damage Covered by Homeowners Insurance? What to Do

Maya Chen

13 May 2026

When bird damage is actually covered

Coverage usually comes down to one question: did a covered peril cause the damage, or did the bird itself cause it? Homeowners policies cover losses from specific listed perils (fire, windstorm, hail, vandalism, and so on under an HO-3's 'open perils' dwelling coverage). If a bird's actions trigger one of those perils, you may have a covered claim.

The clearest example is a window broken by sudden bird impact. If a large bird strikes a window and shatters it, you can argue that the loss resulted from a sudden, accidental event rather than gradual wear, which is the standard the insurer uses to evaluate coverage. Some adjusters will accept this; others will lean on the bird exclusion. The outcome often depends on how you frame and document the claim.

Another covered-peril angle: if nesting materials in a dryer vent or chimney ignite and cause a fire, that fire damage is likely covered because fire is a named peril. The bird is not the covered cause; the fire is. Similarly, if bird activity physically breaks a pipe and water damage follows, the resulting water damage may be covered depending on your policy's water-damage provisions.

What is almost never covered is gradual damage: droppings corroding a roof over years, nest buildup slowly clogging gutters, or woodpeckers working away at siding over months. Insurers treat all of that as a maintenance problem, not a sudden loss.

What actually counts as 'bird damage'

It helps to be specific about what you're dealing with, because the type of damage affects how you frame the claim.

| Damage Type | How It Happens | Coverage Outlook |

|---|---|---|

| Impact damage | Bird strikes window, skylight, or exterior surface at speed, causing cracks or breakage | Possible if framed as sudden/accidental; still subject to bird exclusion |

| Droppings/corrosion | Acidic droppings accumulate on roofing, gutters, HVAC units, or painted surfaces over time | Almost always denied as gradual deterioration and maintenance failure |

| Nesting in vents or eaves | Birds build nests in dryer vents, chimney flues, attic vents, or gutters, blocking airflow or drainage | Generally excluded; only covered if the nest causes a covered peril like fire |

| Nesting-related water damage | Blocked gutters overflow and water penetrates the structure | May be covered if sudden, but insurers often cite maintenance exclusion |

| Pecking/gnawing damage | Woodpeckers or similar birds damage wood siding or fascia boards | Almost always excluded as animal damage and/or deterioration |

Homes with bird feeders face roughly double the risk of bird-window collisions compared to homes without feeders, according to U.S. Fish and Wildlife Service data from 2025. That is worth keeping in mind if you have feeders close to the house and are already dealing with cracked windows.

Why claims get denied: exclusions and limits to know

The bird exclusion is explicit in the policy language. The ISO HO-3 form (HO 00 03 10 00) lists 'birds, vermin, rodents, or insects' directly in Section I exclusions. The HO-5 endorsement form and many state-filed variants like HO-3R carry the same language. When you see that wording, the insurer has a straightforward basis to deny any claim where a bird is the direct cause.

Beyond the bird exclusion, there are two other exclusions that frequently kill these claims:

- Wear and tear / deterioration: Any damage that built up over time, rather than happening in a discrete event, falls here. Corroded flashing from years of droppings is a textbook denial.

- Maintenance exclusion: Insurers, including Liberty Mutual in its published guidance, specifically describe roof damage caused by birds as a maintenance problem, not a covered loss. If your insurer believes you could have prevented the damage with routine upkeep, they will use this.

- Policy sublimits: Even if some coverage applies (say, a broken skylight), you may hit a deductible that exceeds the repair cost, or a sublimit on certain structures.

Texas Department of Insurance and similar state agencies list bird damage and wear-and-tear as among the most common items homeowners insurance simply will not pay for. That is not fine print buried in your policy; it is standard industry practice.

How to check your own policy quickly

Pull out your declarations page and the full policy document (your insurer's app or website portal usually has both). You want to read three specific sections: 'Perils Insured Against' (what is covered), 'Exclusions' (what is not), and 'Loss Settlement' (how they calculate payment). On the declarations page, confirm whether you have an HO-3 or HO-5 form, because HO-5 policies sometimes carry broader open-perils coverage on personal property.

Search the document (Ctrl+F in a PDF) for the words 'birds,' 'animals,' 'vermin,' 'wear and tear,' and 'maintenance.' Read each hit in context to see exactly how your policy words the exclusion. Some state-filed versions word it slightly differently, and a small wording difference can matter during an appeal.

If you want a fast answer without reading the whole document, call your insurer's claims line and ask them to describe how the policy handles bird-related damage before you file. Car insurance claims follow similar coverage logic, but personal auto policies usually exclude damage caused by animals, so check your policy wording before assuming it is covered bird damage. Ask specifically about your scenario: 'If a bird broke a window in a single incident, would that be a covered peril under my dwelling coverage?' Their verbal answer is useful context, but always follow up by locating the written language yourself.

Documenting damage the right way

Documentation is where most policyholders lose claims that they might have won. The goal is to show that a specific, sudden event happened on a known date. Gradual damage has no single event to point to, which is exactly why insurers deny it.

- Photograph everything immediately. Take wide shots showing the whole area and close-ups showing the break, crack, or soiling. Include something in frame that shows scale (a ruler, a coin, your hand).

- Note the exact date and time. If possible, check whether a neighbor's security camera or a doorbell camera captured the incident. Video evidence of an impact event is very strong.

- Keep any physical evidence. If a bird left feathers or was found dead near the impact point, photograph that too. It establishes the bird-collision scenario rather than just 'something broke.'

- Get at least two repair estimates in writing, with itemized line items describing exactly what is damaged and what the repair involves.

- Write a short timeline: when you first noticed the damage, what you observed, whether you saw or heard the impact, and any relevant history (prior inspections, maintenance records showing the area was in good condition).

- If neighbors witnessed the event, get a brief written statement from them with their contact information.

Do not delay. Most policies require you to report claims promptly, and some state statutes specify proof-of-loss deadlines. Florida statutes, for example, include specific proof-of-loss timing requirements. In Washington state, insurers are generally required to finish investigating within 30 days of receiving a claim, and if they cannot, they must notify you in writing and explain why. Knowing your state's rules gives you a timeline to hold your insurer to.

Filing the claim, and what to do if it gets denied

Filing step by step

- Call or file online through your insurer's claims portal as soon as you have documented the damage. Have your policy number, the date of loss, a description of what happened, and your photos ready.

- Ask whether the insurer will send an adjuster to inspect in person. For structural damage, push for an in-person inspection rather than a photo-only review.

- Submit a completed proof-of-loss form if your insurer sends one. Completing it promptly prevents delays in processing.

- Keep a log of every conversation: date, time, name of the person you spoke with, and a one-sentence summary of what was said.

- Ask for the claim decision in writing, including the specific policy language the insurer cites if it denies the claim.

If the claim is denied

First, read the denial letter carefully. The insurer must cite the specific exclusion or reason. If they cite the bird exclusion and you believe the event was a sudden, accidental impact rather than ongoing animal damage, that is your appeal angle. Write a formal appeal letter that: (1) identifies the specific covered peril you are claiming (sudden accidental breakage, for example), (2) cites the exact policy language that applies, (3) attaches all documentation, and (4) argues why the exclusion does not apply to your specific facts.

If the internal appeal fails, most states have an insurance commissioner's office that handles consumer complaints. Filing a complaint is free and creates a formal record. For larger claims, a licensed public adjuster or an attorney who handles insurance disputes can review whether the denial was reasonable. Public adjusters work on contingency and can sometimes negotiate a partial settlement even on a contested claim.

One thing worth noting: if bird damage to a car is part of your situation, the coverage rules are completely different because auto insurance uses a different policy structure (typically comprehensive coverage). After a bird strike while driving, prioritize safety first, then document the incident and damage for your insurer bird damage while driving. The article on whether car insurance covers bird damage covers that scenario in detail. Homeowners and auto policies should not be confused here.

Preventing repeat bird damage

Beyond the claim itself, preventing future bird damage matters both for your property and for the birds. Bird-window collisions are a leading cause of bird mortality, and most are preventable. Using visible deterrents and making windows safer (for example, softening impact if a bird strikes) can help reduce bird-window collisions, as highlighted by blank" rel="noopener noreferrer">Utah State University Extension. BirdSafe Maine (Maine Audubon) recommends reporting birdstrikes and notes that reflective or transparent glass can be hazardous, so deterrents should be applied on the outside surface of windows for maximum effectiveness blank" rel="noopener noreferrer">deterrents must be applied on the outside surface of windows for maximum effectiveness.

- Apply visible patterns to glass surfaces. Audubon recommends spacing markings no more than 2 to 4 inches apart on reflective or transparent glass. The deterrent must be applied on the outside surface of the window to be effective, according to Maine Audubon's BirdSafe guidance.

- Move bird feeders. Place feeders either within 3 feet of a window (so birds cannot build fatal speed before impact) or more than 30 feet away. U.S. Fish and Wildlife data shows that homes with feeders face about double the collision risk.

- Install vent covers and exclusion screens over dryer vents, attic vents, chimney caps, and any other openings where birds might nest. Federal regulations under 50 CFR § 21.14 also specifically identify patching holes and installing exclusion devices as appropriate prevention methods.

- Clean gutters and downspouts at least twice a year to remove nest debris before it causes blockages.

- Inspect your roof, eaves, and fascia boards each spring, which is peak nesting season. Document that inspection with dated photos. This establishes a maintenance record that can help counter a 'failure to maintain' denial if a claim comes up later.

- Use physical deterrents (spikes, slope boards, or reflective tape) on ledges and peaks where birds congregate and deposit droppings. This is especially important near HVAC equipment and roof penetrations.

Good maintenance records do double duty: they protect your property and they give you evidence to push back if an insurer claims the damage resulted from neglect. Dated inspection photos cost you nothing and can change the outcome of a dispute.

FAQ

If my policy excludes “birds,” can I still claim coverage if the bird damage leads to a covered loss like a leak or fire?

Often yes, but you need to frame the sequence as a covered peril that comes after the bird event. For example, if bird activity causes a plumbing breach that then results in covered water damage, focus on the sudden leak and the resulting damage, not the animal activity. If the insurer argues it was ongoing deterioration, use dates, repair invoices, and before and after photos to show it began at a specific point in time.

What counts as “sudden accidental” when a bird breaks something, and how should I describe it?

Try to capture a specific triggering incident (date and approximate time) and the mechanism (impact, nesting material contacting a heat source, bird pecking that immediately caused failure). Avoid vague timelines like “over the last few months.” The closer your description is to a single event, the harder it is for the insurer to characterize the loss as wear and tear.

Does having a “named perils” dwelling policy versus “open perils” change the bird damage answer?

Yes, but it usually only changes the window for arguments. HO-3 dwelling coverage is generally open perils, meaning many direct physical losses are covered unless an exclusion applies. However, the bird or vermin exclusion often still blocks claims when birds are the direct cause. Open-perils personal property can be different, so confirm which sections your policy uses for dwelling versus personal property.

Will replacing a damaged area always be covered if the loss started from a bird strike?

Not automatically. Insurers may cover the physical damage caused by the covered incident but deny additional replacement if they consider it maintenance, rot progression, or a preexisting condition. Ask the adjuster to identify what portion is attributable to the bird-related incident and what portion is attributed to prior deterioration.

If my roof damage is from droppings, is there any way to argue it is not gradual maintenance?

It is difficult because droppings corrosion is usually treated as gradual. Your best chance is to establish a sudden catalyst, such as a localized leak that started after a specific nesting event, or heavy contamination following an event with a known date. Gather evidence like gutter overflow photos, inspection dates, and repair documentation to try to separate sudden failure from long-term neglect.

How do I respond if the insurer denies my claim because “birds caused it,” but the damage appears to be from wind or aging?

Pivot to causation. If windstorm dislodged a loose vent hood after birds nested there, you can argue the windstorm is the proximate cause for the resulting damage. Provide evidence of wind timing (weather records, storm date) and show the bird activity was part of the setup, not the immediate physical cause of the covered loss.

What documentation is most persuasive for bird-related homeowners claims?

Use a timeline package: photos or video of the condition before any cleanup, the date you noticed the damage, the date of the suspected incident, and receipts or estimates for repairs. Also include a copy of any deterrent steps you took (for example, netting installation date or feeder relocation). This helps address both causation and the “maintenance” narrative.

Do I need to report bird damage immediately, and what if I already cleaned it up?

Report promptly even if you have already cleaned. Cleaning does not undo the evidence, but it can reduce what’s left to verify. If you cleaned, document what you removed (photos before cleanup if available) and keep any correspondence with the contractor. Ask the insurer whether they want an inspection before you proceed with repairs.

Can I negotiate a smaller scope settlement instead of a full denial?

Yes, especially for partial losses. If the insurer denies because of the bird exclusion, you can request that they cover the remaining damage that is clearly attributable to a covered peril, like a resulting fire, broken window impact, or sudden water intrusion. Provide line-item estimates that separate the incident-related repair from replacement that looks like maintenance.

What should I look for in the denial letter besides the bird exclusion?

Check whether they cite specific policy wording and whether they dispute the timing of the loss. Many denials hinge on “gradual” versus “sudden,” and on whether they claim the bird activity was the direct cause. If the letter does not identify the exact exclusion language or timeline reasoning, that becomes a useful point in your appeal.

Does the public adjuster or attorney review process differ if the claim is small?

For small claims, it may be faster and cheaper to handle an appeal directly with your insurer and keep documentation tight. Public adjusters and attorneys can still help when the denial involves complex causation or large repair costs, but ask about fees and whether they will pursue partial coverage options if the bird exclusion is asserted.

I have both homeowners and auto policies. If a bird strike damages property, how do I know which policy to use?

Use homeowners insurance for damage to your home and personal property, and auto comprehensive coverage for damage to your vehicle. The coverage logic and exclusions differ, so don’t submit the same incident to both without clarifying what each policy covers. If a bird caused a chain reaction (for example, it broke a window and that led to interior damage), homeowners is usually the right path.